Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

=

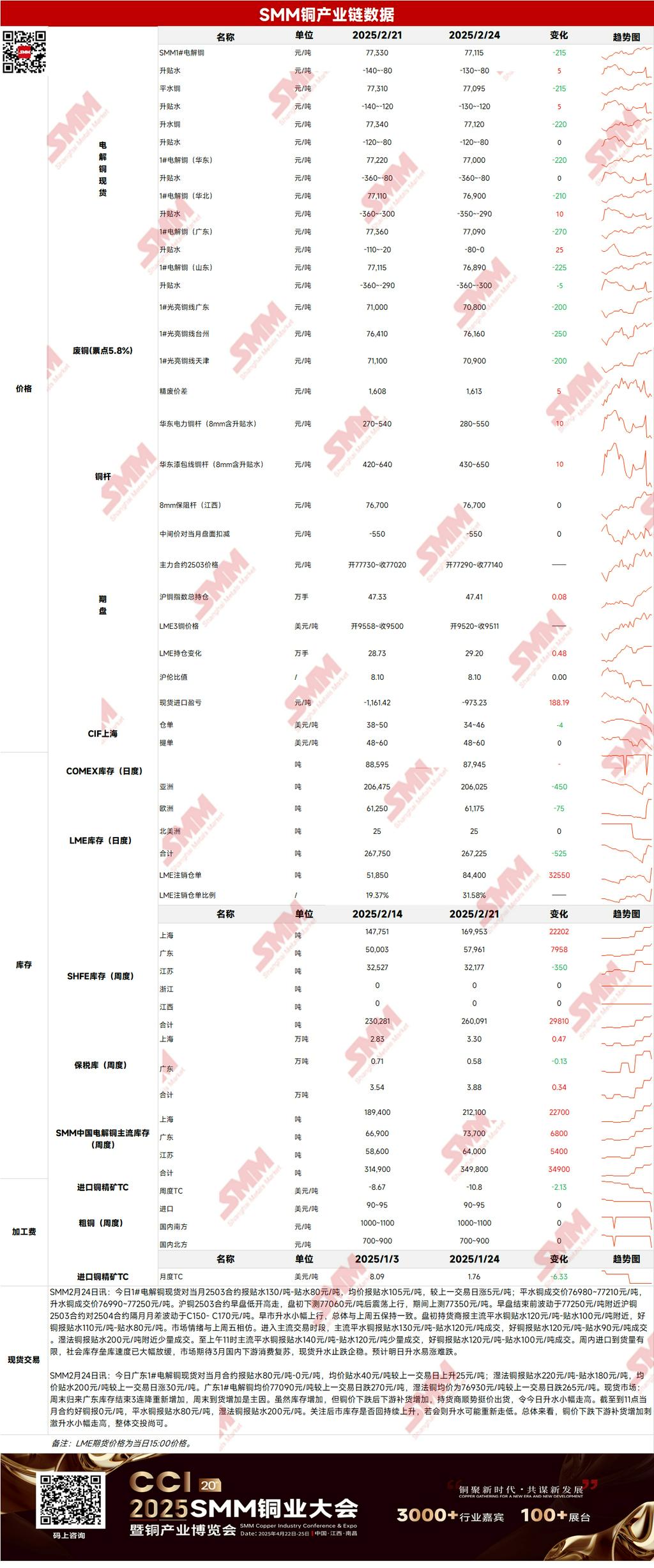

Futures Market: Overnight, LME copper opened at $9,490.5/mt, rose to an intraday high of $9,531/mt at the beginning of the session, then declined to a low of $9,474/mt. By the end of the session, the center rebounded but later returned to the low level, closing at $9,502/mt, down 0.14%. Trading volume reached 16,000 lots, and open interest stood at 291,000 lots. Overnight, the most-traded SHFE copper 2504 contract opened at 77,360 yuan/mt, hit an intraday high of 77,580 yuan/mt early in the session, fluctuated downward to a low of 77,160 yuan/mt during the session, and fluctuated rangebound at the end, closing at 77,300 yuan/mt, down 0.15%. Trading volume reached 24,000 lots, and open interest stood at 173,000 lots.

[SMM Copper Morning Meeting Notes] News: (1) Recently, a large number of LME warehouse warrants in Asia were cancelled. As of February 24, 2025, cancelled warrants totaled 28,200 mt in Kaohsiung, 24,800 mt in Gwangyang, and 18,175 mt in Busan, accounting for 31.58% of total inventory.

Spot: (1) Shanghai: On February 24, mainstream standard-quality copper was quoted at a discount of 130-120 yuan/mt against the front-month contract, and high-quality copper was quoted at a discount of 120-80 yuan/mt. Limited import arrivals during the week and a significant slowdown in inventory buildup in the social warehouses led the market to anticipate a recovery in domestic downstream consumption in March. Spot premiums stabilized after the decline and are expected to be more likely to rise than fall tomorrow.

(2) Guangdong: On February 24, #1 copper cathode spot in Guangdong was quoted at a discount of 80-0 yuan/mt against the front-month contract, with an average discount of 40 yuan/mt, up 25 yuan/mt from the previous trading day. Hydro copper was quoted at a discount of 220-180 yuan/mt, with an average discount of 200 yuan/mt, up 30 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 77,090 yuan/mt, down 270 yuan/mt from the previous trading day, while hydro copper averaged 76,930 yuan/mt, down 265 yuan/mt. Overall, the decline in copper prices stimulated downstream restocking, slightly pushing up premiums, with moderate trading activity.

(3) Imported Copper: On February 24, warehouse warrant prices ranged from $34 to $46/mt, QP March, with the average price down $4/mt from the previous trading day. B/L prices ranged from $48 to $60/mt, QP March, with the average price unchanged from the previous trading day. EQ copper (CIF B/L) was quoted at $0-8/mt, QP March, with the average price down $2/mt from the previous trading day. Quotes referenced cargoes arriving in mid-to-early March. During the day, some suppliers rushed to sell due to narrowing spreads, causing warehouse warrant prices to continue falling. Quotes for early March registered B/L remained firm but saw limited transactions. Overall, market divergence was evident.

(4) Secondary Copper: On February 24, secondary copper raw material prices fell by 200 yuan/mt MoM. Guangdong bare bright copper prices ranged from 70,700-70,900 yuan/mt, down 200 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 1,613 yuan/mt, up 200 yuan/mt MoM. The price spread between primary and secondary copper rods was 965 yuan/mt. According to an SMM survey, Ningbo customs clearance companies reported receiving a small number of orders for secondary copper raw materials imported from the US. Following China's first round of countermeasures against US imports, which excluded secondary copper raw materials, importers have begun small-scale imports, with the possibility of increased procurement of US secondary copper raw materials in the future.

(5) Inventory: On February 24, LME copper cathode inventory decreased by 525 mt to 267,225 mt. SHFE warrant inventory decreased by 319 mt to 153,766 mt.

Prices: Macro side, Russian President Vladimir Putin stated that Russia and the US could agree to cut armaments by 50%, and Russia plans to resume aluminum product exports to the US, with an export volume of 2 million mt. Meanwhile, concerns over US economic growth have begun to emerge, exacerbated by the approaching deadline for Trump's tariffs on Canada and Mexico next week, leading to a decline in copper prices. Fundamentals side, limited import arrivals during the week, coupled with increased downstream restocking amid falling copper prices, significantly slowed the pace of inventory buildup in social warehouses. As of Monday, February 24, SMM data showed copper inventories in major regions nationwide increased by 16,000 mt WoW to 374,000 mt, with total inventory up 208,000 mt from the pre-holiday level of 166,000 mt. Among them, Shanghai inventory was 128,000 mt higher than the pre-holiday level, Guangdong inventory was 48,000 mt higher, and Jiangsu inventory was 37,000 mt higher. Price-wise, copper prices are expected to continue declining today.

[The information provided is for reference only. This article does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.]

For queries, please contact William Gu at williamgu@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn